United States remittance tax: How is the 1% fee applicable?

Major points

-

Beginning January 1, 2026, the United States introduced a 1% tax on certain international money transfers. The Trump administration.

-

The tax only applies to transfers funded with cash, money orders, or cashier's checks.

-

Transfers funded from a U.S. bank account, debit card or credit card are exempt.PT from the tax.

-

The money transfer provider automatically collects the tax, so senders do not have to file additional paperwork.

-

The tax applies regardless of citizenship or immigration status.

-

The simplest way to avoid the tax is to send money digitally using a debit card or bank account.

What is a remittance and why is it important?

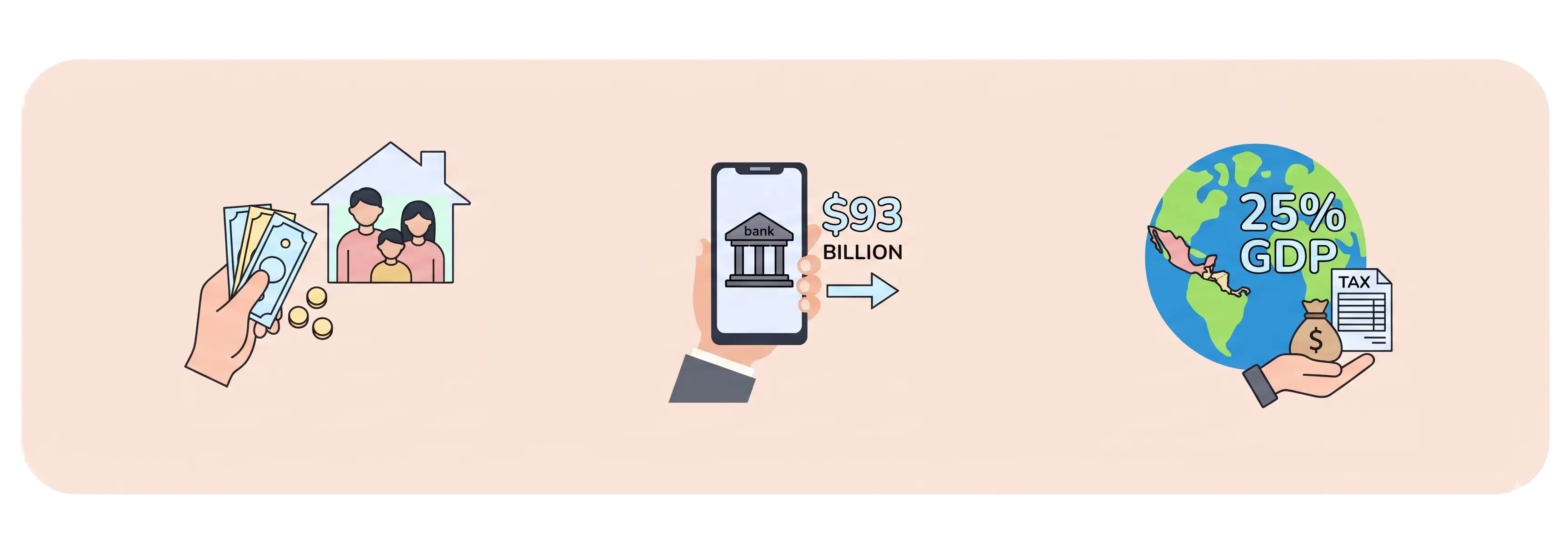

If you have ever sent money to a family member living in another country, perhaps to assist with rent, medical expenses, or school fees, you have made a remittance. Simply put, a remittance is money sent from an individual residing in one country to an individual residing in another country.

For millions of families worldwide, remittances serve as a vital financial lifeline. The United States is the largest source of remittances globally, sending approximately $93 billion abroad each year. The top recipients of U.S. remittances include Mexico, India, Guatemala, the Philippines, and China. In several of these countries, remittances represent a substantial share of gross domestic product (GDP), e.g., in Honduras and El Salvador, remittances account for around 25% of GDP.

For millions of families worldwide, remittances serve as a vital financial lifeline. The United States is the largest source of remittances globally, sending approximately $93 billion abroad each year. The top recipients of U.S. remittances include Mexico, India, Guatemala, the Philippines, and China. In several of these countries, remittances represent a substantial share of gross domestic product (GDP), e.g., in Honduras and El Salvador, remittances account for around 25% of GDP.

For the first time, the U.S. Government is now taxing certain types of these transfers. Below is information regarding the new tax and its implications.

What is the new 1% remittance tax?

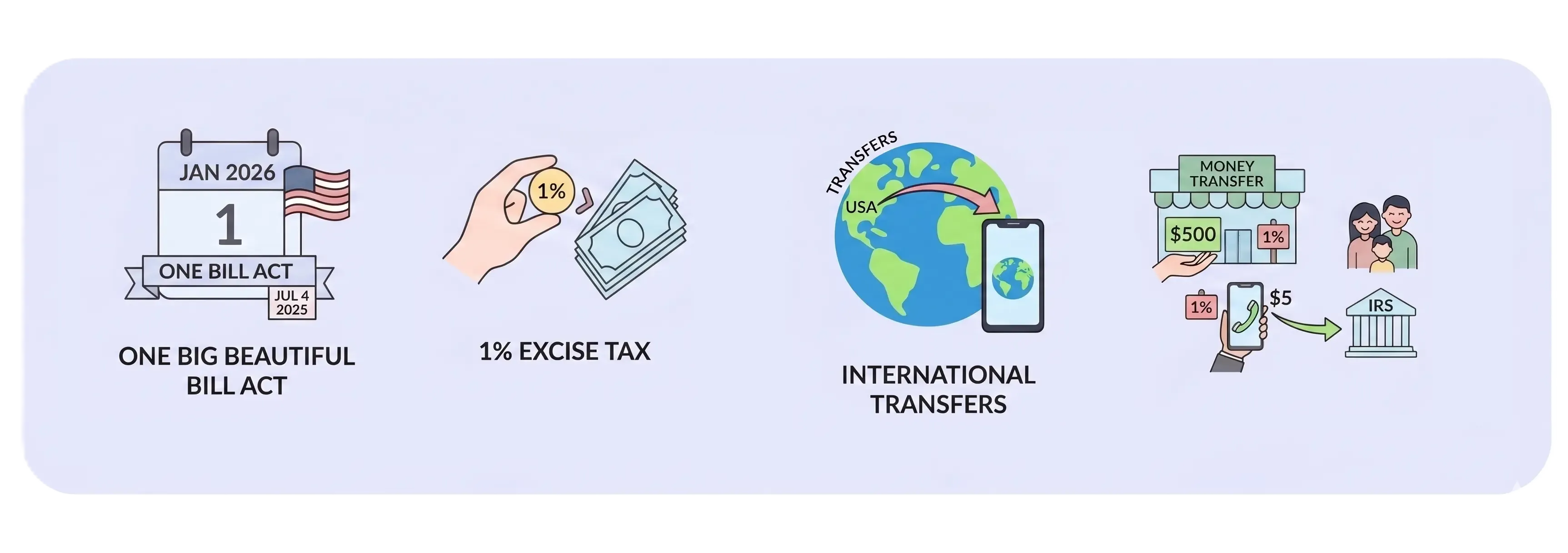

Starting January 1, 2026, a 1% excise tax applies to certain international money transfers originating from the United States. This tax was introduced through the One Big Beautiful Bill Act, signed into law on July 4, 2025. An excise tax is a tax levied to a specific activity, in this instance, sending money abroad using cash or other physical payment methods.

An example scenario: if you visit a money transfer store and send $500 in cash to a family member overseas, the money transfer company must collect an additional $5 (1% of $500) and remit it directly to the IRS.

An example scenario: if you visit a money transfer store and send $500 in cash to a family member overseas, the money transfer company must collect an additional $5 (1% of $500) and remit it directly to the IRS.

Who does this tax apply to?

One of the most frequently asked questions is who must pay this tax. The answer may come as a surprise to many. The tax applies to everyone, regardless of your citizenship or immigration status. Earlier drafts of the legislation proposed exemptions for U.S. citizens and green card holders, but those were ultimately removed from the final bill.

Therefore, whether you are a U.S. citizen, a lawful permanent resident (green card holder), a temporary worker holding a valid visa, or undocumented, if you send a qualifying cash-based transfer you will be subject to the tax. However, any transfers under $15 are exempt due to a small-value exclusion included in existing federal laws designed to protect consumers.

Which transfers are subject to the tax which are exempt?

The tax depends entirely on how the transfer is funded, not who sends it.

Here is a simple summary of what is and isn't taxable:

Transfers subject to the 1% tax

- Cash transfers made at a money transfer location

- Cashier’s check

- Money order

Transfers that are exempt

- Debit card payments using a U.S.-issued card

- Bank wires from a U.S. bank account

- Credit card payments using a U.S.-issued card

- Cryptocurrency or stablecoin transfers

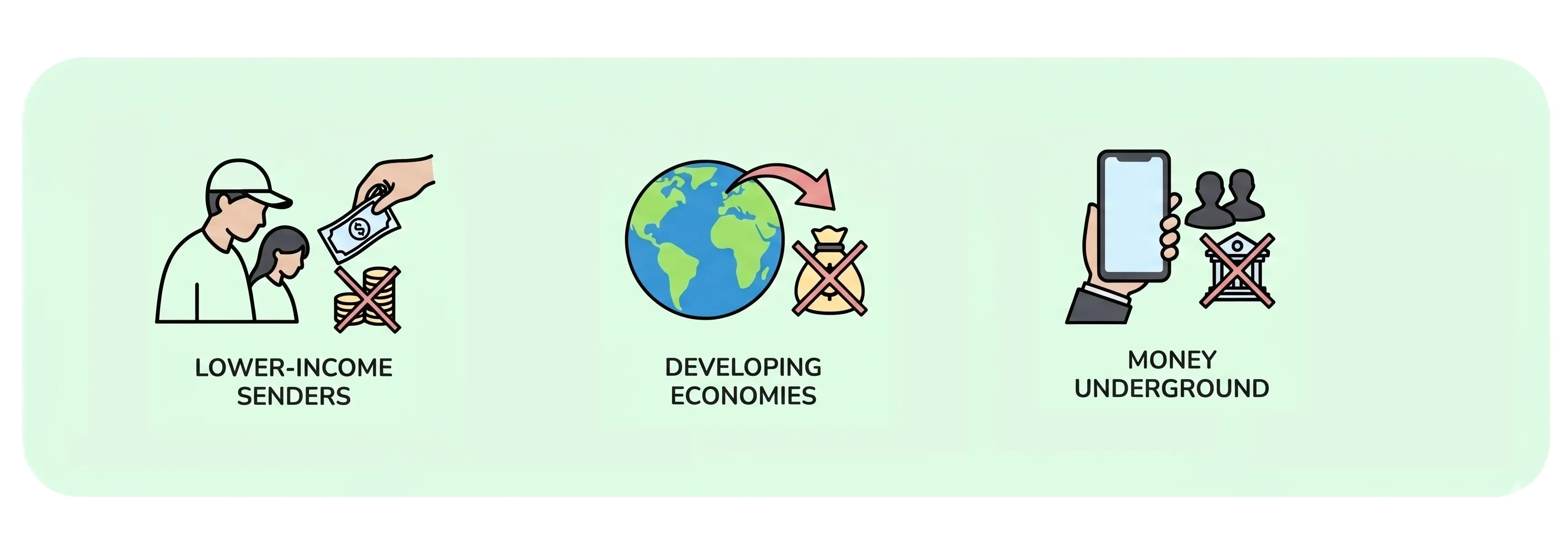

In short, cash is taxable; digital/bank-funded is non-taxable. The distinction is important because cash transfers are generally used by individuals who do not have access to traditional banking services, including many low-income individuals and immigrant communities.

How is the tax assessed? Must I file any documentation?

No, you do not have to file any paperwork or take additional steps. The money transfer company (also referred to as the “remittance transfer provider”) is legally responsible for collecting the tax at the time of the transaction and send the tax to the IRS. The tax will be reflected as a separate charge on your transfer receipt.

How much additional will I pay?

The calculation is straightforward; it is simply 1% of the amount sent:

$300 transfer = $3.00 tax

$500 transfer = $5.00 tax

$1,000 transfer = $10.00 tax

Although 1% may seem small, the cost can add up quickly for those who send money frequently. For example, for someone transferring $500 per month, the tax amounts to $60 per annum.

Why are people concerned?

Policymakers and experts across the entire political spectrum have raised concerns about the potential impact of the tax:

Cash-based money transfers are primarily used by individuals without bank accounts and by others with financial constraints. Imposing a tax on foreign remittances effectively taxes those least able to absorb increased costs.

Some countries rely heavily on remittance inflows. According to the Center for Global Development, Mexico alone may experience a decline in remittance income of over $1.5 billion annually.

Organizations such as the Tax Foundation note that the tax is “difficult to enforce” because informal transfer systems may emerge outside regulated financial channels. One survey indicates that a large portion of Latino immigrants would consider using informal or underground channels if transfers become more expensive.

Many Americans who send money to relatives abroad were surprised that the final law removed exemptions for U.S. citizens and permanent residents.

How BOSS Money can assist you in making smarter money transfers

The easiest way to avoid the 1% remittance tax is to send money digitally instead of using cash. Funding your transfer with a U.S. bank account or U.S. debit or credit card means the transfer will not be subject to the 1% tax.

Since 2013, BOSS Money has helped immigrant communities send money to family members around the world. BOSS Money currently has over 1 million active customers and processes more than $6.3 billion in annual transactions to 50+ countries, with over 250,000 cash pick up locations. By sending money digitally through BOSS Money, customers can avoid the 1% remittance tax while benefiting from:

- Competitive exchange rates with no hidden fees

- Transfers to 50+ countries

- 250,000 cash pick up locations worldwide

- Transfers that often arrive within minutes

- A highly-rated mobile app(4.8 stars) available on iOS and Android devices

- New customers receive 5 $0 fee transfers to Mexico and 3 $0 fee transfers to all other countries

Learn more and/or download the app at bossmoney.com.

Laws regarding the U.S. transfer of money overseas frequently asked questions

Is the 1% tax applied to the transfer fee or the amount sent?

The tax is 1% of the total amount you’re sending, not the transfer fee. If you send $400, you’ll pay $4 in tax on the money sent.

Am I exempt if I am a U.S. Citizen?

No, the final law removed the exemption for U.S. citizens and green card holders. The tax applies to all qualifying cash-based transfers, regardless of immigration status.

Do I pay tax if I send money via the BOSS Money app using my debit card?

No, you will not pay the 1% tax. Transfers funded by a U.S.-issued debit card, credit card, or bank account are specifically excluded from the tax. Only transfers utilizing cash and/or physical payment mediums (i.e., money orders, cashier’s checks) will be taxed.

Does the recipient of the money pay the tax?

No, the tax is paid by the sender in the United States and collected before the transfer is completed. The intended recipient will receive the original amount of the transfer.

Can I dispute the tax and receive a refund?

Currently, there is no provision for a refund of the excise tax. The simplest solution is to fund your transfer digitally, i.e., from your bank account, debit card, or credit card, rather than using cash.

Conclusion

Because regulations may continue to evolve, we recommend staying up to date with the IRS and/or consulting a tax professional for guidance on any specific questions related to your situation.

Sources: all third party information obtained from applicable website as of April 15, 2026

This article is provided for general information purposes only and is not intended to address every aspect of the matters discussed herein. The information in this article is not intended as specific personal advice. The information in this article does not constitute legal, tax, regulatory or other professional advice from IDT Payment Services, Inc. and its affiliates (collectively, “IDT”), and should not be taken or used as such by any individual. IDT makes no representation, warranty or guaranty, whether express or implied, that the content in this article is current, accurate, or complete. You should obtain professional or other substantive advice before taking, or refraining from, any action on the basis of the information in this article.