What is the cheapest way to send money internationally in 2026?

When you regularly send money home, transfer fees and related charges slowly compound. An $8 total charge on a $100 monthly transfer amounts to $96 a year—nearly a month’s worth of remittance. Imagine how much more of your hard-earned money you’re losing if you’re sending higher amounts?

This guide helps you find the cheapest way to send money internationally in 2026. We explore the cheapest, most reliable, and fastest ways to send money using real up-to-date data on costs, speeds, and security of digital platforms like PayPal, Wise, and BOSS Money.

We’re also making it easier for you to choose from the cheapest international money transfer providers by comparing their fees and exchange rates.

Quick answer: Overview of the cheapest international money transfers

For small transfers, digital apps provide convenience and lower fees. For large amounts, foreign exchange specialists typically offer the best rates and most secure platforms. For urgent transfers, service providers with global networks allow instant transfers.

What determines the real cost

A transfer with ‘zero fees’ can still be expensive due to exchange rate markup and other charges.

The total cost of sending money abroad depends on multiple factors, including:

- Currencies for sending and receiving

- Source and destination countries

- Amount of money sent

- Payment method (debit, credit, bank, wire, etc.)

- Delivery option (cash pickup, bank transfer, mobile wallet, etc.)

Currency conversion fees and markups

Money transfers involving different currencies are typically subject to currency conversion fees and may include hidden markups.

buyers and sellers are willing to pay for the currency. But instead of this rate, many banks and money transfer services give customers a lower exchange rate.

The problem with this system is that the hidden markup can cost more than the visible transfer fee. It’s also not always clearly disclosed before a transfer is confirmed, leaving senders and recipients shocked at how much less actually arrives.

Payment method and delivery options

For digital apps that support wallets, transfers are often free when made from the balance. Some money transfer services also waive charges when senders link their debit cards or bank accounts. Payments made with credit cards often incur additional charges. Some delivery methods, such as home delivery or bank transfer, may also incur additional charges.

Comparison of transfer methods

There are many different ways to send money internationally without fees. These include digital apps, banks, and cash services. The best method depends on what you prioritize: low cost, convenience, or speed.

Digital apps

Digital apps like BOSS Money, Wise, Xoom, and Remitly are often the cheapest and fastest, especially for regular remittances or smaller amounts. The fees are typically low, with transparent pricing. Transfers are instant or take no more than a few hours.

Banks

Banks with global networks are generally more secure. When sending money within the same bank systems, transfer fees are often waived. However, transfers outside of the bank system usually come with higher fees and longer transfer times.

Cash services

Money transfer providers like Western Union, MoneyGram, and other money transfer service providers with physical locations worldwide allow you to send money for cash pickup. They’re useful in areas where people don’t have access to banks or mobile wallets. Although transfers are instant or within the same day, they often incur higher fees and exchange rate markups.

Provider cost and feature comparison table

Here’s a quick view of how the different providers stack up. The costs shown below are based on an instant transfer of $100 to Mexico paid through a debit card for cash pickup.

| Service provider | Total fees | FX rate (1 USD) |

Speed | Best for |

|---|---|---|---|---|

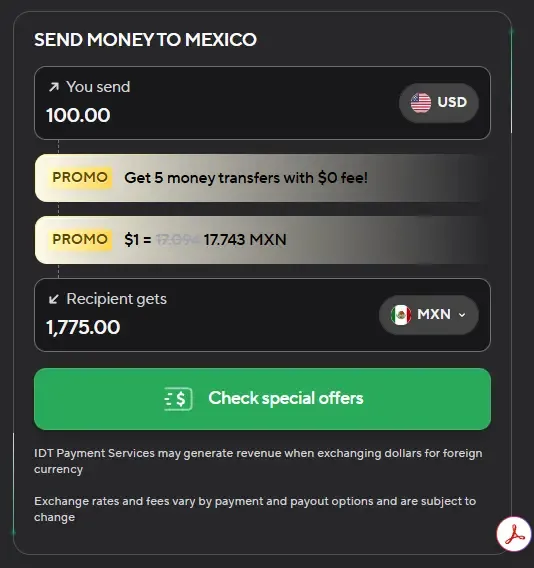

| BOSS Money | $0 | 17.743 MXN | Within minutes | Immigrants and expats regularly sending money abroad |

| Wise1 | $2.79 | 17.3401 MXN | 30 minutes to next day | Businesses with remote workers |

| Remitly2,3 | $1.99 | 17.69 MXN | Within minutes | Small business owners |

| Traditional banks4-7 | $6 to $35+ | 17.1529 MXN | 2 to 7 days | Large business owners and high-value senders |

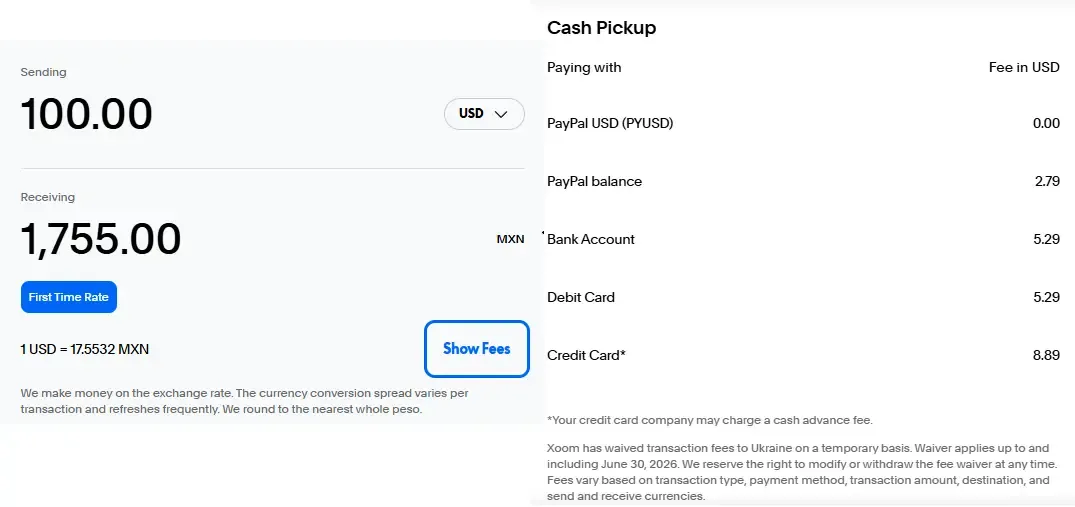

| PayPal/Xoom8-11 | 5% international fee (maximum of $4.99) + 4.00 MXN fixed receiving fee + 4.00% currency conversion spread |

17.5532 MXN | Within hours | Small to large business owners |

*Based on published rates on April 23, 2026.

Hidden costs and real-world examples

Some banks and money transfer service providers may claim “no fee on any transfers,” but this claim may be limited to just “sending” fees. They do not include currency conversion fees, exchange rate markups, card fees, and receiving fees.

When these charges are deducted from the receiving amount, the sender may not always be aware these charges were incurred. They only find out when the recipient gets an amount lower than expected.

In Xoom and PayPal, for example, aside from the percentage-based international fee, there is also a fixed receiving fee or a currency conversion fee. If currency conversion is involved in the transaction, up to 4% of the converted amount is charged.

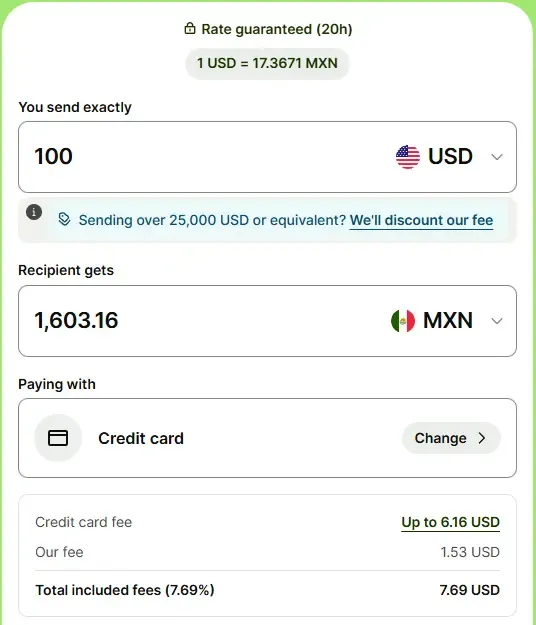

The fees on Wise are pretty similar. When you send $100 using a credit card, the transfer amount is deducted a credit card fee of up to $6.16 and a Wise transfer fee of $1.53. The recipient gets only 1,603.16 MXN.

Source1

Cheapest options by typical transfer scenarios

Most migrant workers send approximately 15% of their income back home12-14. For most, that comes to about $200-$300 a month.

To make it easier to compare which money transfer option is cheapest, here’s a table that shows how much recipients can get when someone sends $1,000 with a debit card through digital platforms.

| Sending USD 1,000 | to Mexico (MXN) |

to Nigeria (NGN) |

to Venezuela (VES) |

|---|---|---|---|

| BOSS Money* | 17,661.00 | 1,407,831.00 | 575,029.00 |

| Wise**1 | 17,080.30 | 1,343,955.57 | -not supported- |

| Remitly*** | 17,730.002 | 1,387,095.0015 | 616,870.0016 |

| PayPal8-11/Xoom17,18 | 17,612.00 | 1,346,214.30 | 479,230.91**** |

*For new users eligible for $0 transfer fee and promotional exchange rates for the first 3 to 5 transfers.

**Debit card fee ($12.35) and transfer fee ($6+) deducted from the transfer amount.

***Based on promotional rates for the first money transfer.

****Xoom does not support transfers to Venezuela. Rates based on direct PayPal to PayPal wallet transfers only.

Although Remitly appears to give more value, these rates are only for the first money transfer. For successive transfers, BOSS Money still delivers the highest rates and lowest fees.

Cheapest by scenario

Check these recommendations based on common transfer scenarios:

Small transfers

Digital apps like BOSS Money and Wise are among the cheapest options. They offer low fees, transparent exchange rates, and fast transfers. For small, regular transfers, these platforms often waive fees or offer promotional rates, making them ideal for frequent senders and monthly remittances by immigrants and expats.

Large transfers

When sending larger amounts, FX brokers usually offer the best exchange rates and lowest fees. These brokers focus on providing competitive rates for substantial sums and may offer specialized services for businesses and individuals who regularly send high-value transfers.

Urgent transfers

Services like BOSS Money, Remitly, Xoom, and Western Union are ideal for instant transfers. They charge higher fees but provide fast delivery—within seconds or minutes—making them great for sending money in emergencies.

Recipients without bank accounts

Cash pickup options from Western Union, MoneyGram, or BOSS Money are best for those without access to a bank or mobile wallet. These services offer instant or same-day availability.

Payment and delivery methods that affect cost

Payment and delivery methods affect the total transfer cost.

Usually the cheapest method, as it avoids the additional charges of credit cards. Some platforms may even offer free transfers when linked to a bank account. However, transfers can take longer (2-3 days).

Faster, but usage comes with a steep price. Expect to pay higher fees, usually 3-5% on top of the transfer fee, and interest charges from the credit card company. This method is best for those who need quick transfers but are willing to pay for the convenience.

Cash pickup methods are usually the most expensive, with both high service fees and exchange rate markups. However, they’re a lifeline for recipients without bank accounts. For emergencies, these methods are invaluable but often come at a higher price

When choosing the cheapest international money transfer, choose one that offers multiple payment and delivery options. BOSS Money, for instance, allows senders to pay for the transfer through debit card, credit card, mobile wallet, and bank transfer. Recipients get the money transfer through cash pickup, mobile wallet, bank deposit, or home delivery.

Also, ensure that the provider is transparent about all related charges. Boss Money, for example, ensures transparency by clearly outlining all exchange rates and fees before the sender confirms the transaction.

You can download the app and create an account without sign-up fees. The first five money transfers are free, and subsequent transfers using a debit card are also fee-free. Moreover, first-time users receive promotional exchange rates, so the amount the recipient receives is higher than that from other money transfer service providers.

Practical tips for minimizing international transfer costs

Compare providers

Different providers have different rates and fees based on the source and destination countries. Be sure to compare the total cost, including transfer fees, exchange rates, and receiving fees, to find the provider that offers the best deal for your specific transfer. Most money transfer services have online calculators to give senders an idea of the total costs.

Avoid credit card payments

Transfers paid through credit card incur higher charges. Aside from the platform fees, the credit card company may also impose cash advance fees and other charges. When possible, use a debit card, a linked bank account, or an in-app wallet to avoid those additional charges.

Use mid-market rate services

Choose a money transfer service that offers the mid-market rate. This fair, market-driven rate has no currency conversion markups. Apps like BOSS Money and Wise, known for their transparent pricing, offer this rate with no hidden markups, so you’re sure to get a good deal.

Check promotions

Look for special offers or promotions that can help you save on fees. Many money transfer services, such as BOSS Money, frequently offer waived transfer fees, bonus exchange rates, and other promos that can significantly increase the amount of money received.

What is the cheapest way to send money internationally?

Digital apps with no sign-up or subscription fees are usually the cheapest way to send money internationally. BOSS Money, in particular, can be downloaded and used for free. It also offers high exchange rates and low transfer fees.

Can I send money internationally without fees?

Yes, you can. Choose a reliable money transfer app that allows free transfers using debit cards or in-app wallets, and that uses mid-market exchange rates at no markups.

Are banks more expensive for international transfers?

Yes, banks are generally more expensive. While transfers within the same bank system may have lower fees, most traditional banks quietly eat up 4 to 10 percent of each transfer.

What is the easiest way to send money abroad?

The easiest way to send money abroad is to download a money transfer app, like BOSS Money. Digital apps can be used on mobile and linked to debit cards for fast and affordable international money transfers.

Which transfer method is fastest?

International money transfers made through digital platforms are typically the fastest, with funds available to the recipient instantly or within just a few minutes.

Sources: all third party information obtained from applicable website as of April 28, 2026

- https://wise.com/us/pricing/send-money

- https://www.remitly.com/us/en/currency-converter/usd-to-mxn-rate

- https://www.remitly.com/us/en/help/article/costs

- https://www.us.hsbc.com/international-banking/global-money-transfers/#fn-exchrate60sec

- https://www.wellsfargo.com/international-remittances/mexico/

- https://www.wellsfargo.com/international-remittances/cost-estimator/

- https://www.citi.com/online-services/wire-transfers

- https://www.paypal.com/us/digital-wallet/send-receive-money/send-money-internationally/send-money-to-mexico

- https://www.paypal.com/us/digital-wallet/paypal-consumer-fees

- https://www.paypal.com/us/digital-wallet/send-receive-money/send-money-internationally

- https://www.xoom.com/mexico/send-money

- https://www.un.org/ht/desa/remittances-matter-8-facts-you-don%E2%80%99t-know-about-money-migrants-send-back-home

- https://www.imf.org/en/publications/fandd/issues/series/back-to-basics/remittances

- https://ourworldindata.org/great-global-redistributor-money-sent-brought-back-migrants-remittances

- https://www.remitly.com/us/en/currency-converter/usd-to-ngn-rate

- https://www.remitly.com/us/en/currency-converter/usd-to-ves-rate

- https://embed.xoom.com/nigeria/send-money

- https://www.paypal.com/us/digital-wallet/send-receive-money/send-money-internationally/send-money-to-venezuela

This article is provided for general information purposes only and is not intended to address every aspect of the matters discussed herein. The information in this article is not intended as specific personal advice. The information in this article does not constitute legal, tax, regulatory or other professional advice from IDT Payment Services, Inc. and its affiliates (collectively, “IDT”), and should not be taken or used as such by any individual. IDT makes no representation, warranty or guaranty, whether express or implied, that the content in this article is current, accurate, or complete. You should obtain professional or other substantive advice before taking, or refraining from, any action on the basis of the information in this article.